| |

|

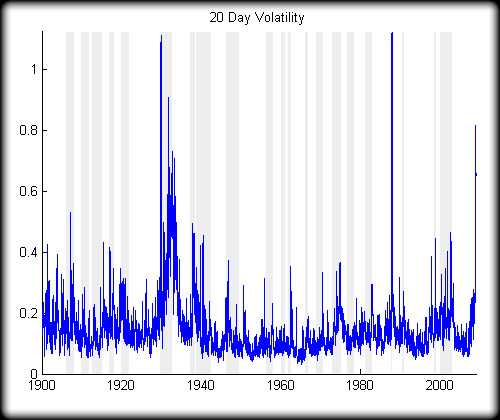

A New Old Kind of Volatility

Don’t be too quick to swallow all of those analyses that compare the SP500 or Dow Jones Industrials to 1974. Although I rarely see it mentioned, there is substantial evidence that our current market may be more similar to the 1930’s than to the 1970’s. The level of uncertainty today is an order of magnitude higher than it was in the 70’s.

The bear markets of the 70’s never saw price swings such as

those occurring on a daily basis today. Consider the chart below displaying

the 20-day historical volatility of the Dow since 1900. In 1929, something

truly extraordinary happened. Traders became extremely uncertain about

the future of the stock market. One day would see incredible panic selling

only to be followed within a day or two by a massive buying frenzy.

Price was being pushed back and forth in a wild game of warfare where

most players took large risks. Does that sound familiar?

Volatility during the bear markets of the 70’s peaked at 0.36 on October 23, 1974. On October 31, 2008 volatility reached 0.82.

Since the beginning of daily record keeping this type of event has only occurred twice! The highest volatility occurred on November 21, 1929 at 1.11. 1929 was the beginning of a several year period where the stock market maintained outrageous volatility levels. Volatility was still above 0.4 in late 1933. This was the start of a world wide 25 year secular bear market in equities. 1929 was accompanied by much economic justification for the uncertainty, most notably an overheated bull market with rampant speculation fueled by easy credit.

The October 19, 1987 crash referred to as Black Monday yielded a one day drop in the Dow of 22%. This day of intense movement triggered a volatility spike to 1.12 on November 12, 1987. This time things were very different from the 30’s. The world was in a secular bull market and there were no significant economic justifications for the ’87 crash. Wikipedia states ”Potential causes for the (1987) decline include program trading, overvaluation, illiquidity, and market psychology.” Notice that none of these are directly related to the economy. Robert Schiller has also done much research on the reason for the ’87 crash. He found no economic cause and noted that many investors sighted the declines of the former week as their reason for selling. The crash only lasted one day and the entire bear market duration was less than 2 months. The elevated volatility was a flash in the pan and disappeared as fast as it arrived.

Today the Dow Jones Index has returned to these extreme volatility levels. Similar to the 1930’s we are in a secular bear market and there are tremendous economic and credit market problems mounting ever higher to justify the drop in asset prices. It is a full 2 months after the dizzying free fall in October and we are still living in an extreme volatility environment. The rate of market fluctuations in the 70’s didn’t approach what we have seen in recent months. We may be witnessing the beginning of sustained volatility. History may not be a crystal ball for predicting the future, but it makes us aware of what CAN happen. Anyone claiming that a worldwide depression is impossible in the current day in age is simply displaying their ignorance of human psychology, its affects on capital markets, and its relationship to the economy.

Bradley Okresik

12/08